If you’ve considered opening a small business, we’ve got a good feeling that 2024 is your year. Despite worries over inflation and high-interest rates, the U.S. economy continues to grow.

And while entrepreneurs are concerned with inflation (78%), interest rates (65%), and commodities prices (63%), there’s still good news to be had. Sixty-six per cent of small businesses in the U.S. are currently profitable, and 76% feel that they’ll continue to stay open and profitable through the current socio-economic situation. If that’s the inspiration you’ve been looking for, well, you’ve come to the right place.

Starting a successful business in 2024 is about starting on the right foot. With the seven steps we’re sharing, you’ll have everything you need to get your business off the ground and on its way to becoming profitable.

What’s a good small business to start in 2024?

When you’re thinking about what kind of business to start, you need to consider about two main factors:

- Does your business fill an unmet consumer need in your area?

- Are you passionate about your business and do you have a level of expertise in your business?

If you can solve a problem for people while doing something that you enjoy, you’ve found the perfect recipe for a successful business. Of course, having a great idea and passion for your business is the ideal place to start—but where do you go from there?

What do you need to start a small business?

Whether you’re opening a brick-and-mortar retail store or a service-based business, all businesses need to start at the same place. Taking time at the beginning to get all of your ducks in a row is the best way to build a solid foundation and will help you ensure your business will survive long term.

No matter what kind of business you’re thinking of, when you’re starting out, there are some basic things you’ll need to get started.

Important things to think about:

- Market, competitor, and location research

- A business plan

- Funding

- A bank account

- Employer identification number (EIN)

- Business location

- Business structure (will you function as a corporation, LLC, sole proprietor, etc.?)

- Business insurance

- Licenses and permits as they apply to your business

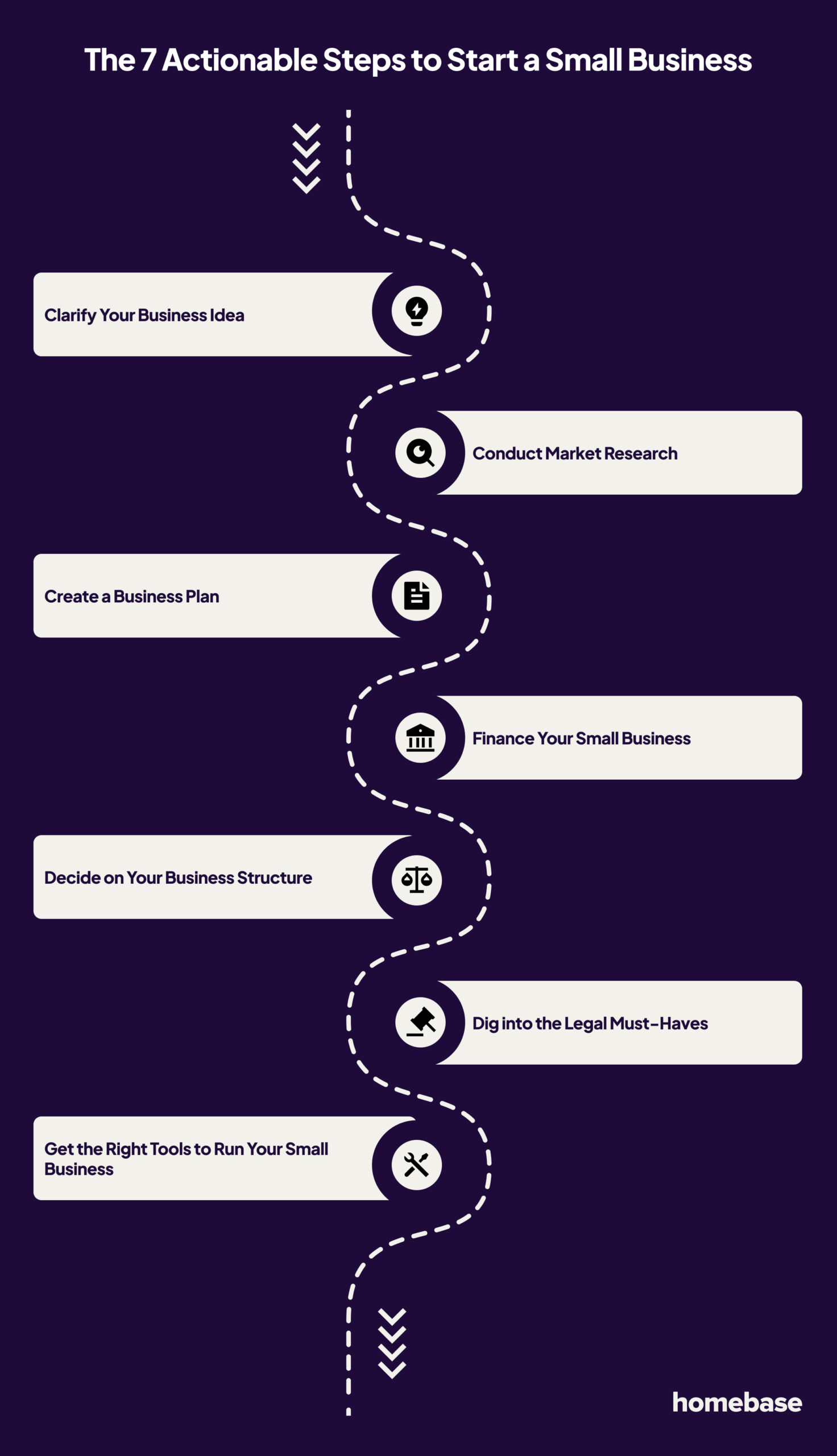

How to start your small business in 7 steps

Every business is different, that’s for sure. But there are some things that every business will need to do to get started. These seven actionable steps will help you start your next small business.

Step 1: Clarify your business idea

If you’ve decided you want to start a new business, but you still need to figure out what that business should be, brainstorming business ideas is the best place to start.

As mentioned above, finding something you’re passionate about that also fills a need in the market is a great starting point for any business. The final element is something that you can monetize. You may be passionate about books but aren’t a great writer. So, you pivot to opening a bookstore… One problem: your small town already has two independent bookstores. The solution? You decide to open a bookstore in another town. Now, you’ve found something you’re passionate about that fills a need and is profitable.

If you don’t have a set idea of what kind of small business you want to open, try answering a few of these questions:

- What do you love doing?

- What would you rather not spend your time doing?

- What are you good at?

- What are you passionate about?

- When friends and family ask you for advice, what questions are they asking?

- If you had to talk about a topic for five minutes on the spot with no preparation time, what would it be?

The answers to these questions can show you where to focus your business. And if you already have a business idea, these answers can help you expand on that idea. Whatever idea you have, always ask yourself if it’s something that’s needed and if you’re good at it.

Step 2: Conduct market research

A critical step in starting any business is market research.

Market research shows whether your idea can become a profitable, successful business. It gives you insights into how your business will perform and can help mitigate some risks associated with starting a new small business.

Market research is made up of two types of research, primary and secondary information:

- Primary information is any information you gather directly from consumers. This could take the form of focus groups, surveys, telephone interviews, and questionnaires that you administer to your target market.

- Secondary information is any information you gather from external sources. This could take the form of government census data, research reports, polling results, and research conducted by other businesses in your industry or location.

While gathering primary information is more time-consuming and expensive than secondary information, the best market research uses both primary and secondary information.

Market research helps your business in a variety of ways:

- Validate your business idea: Market research helps you determine if your business idea is profitable.

- Get a better understanding of your customers: For demographics like age, location, and education level, market research can deliver important information about your would-be customers.

- Find your unique value proposition: When you look closely at your competitors and their actions, you can find what sets your business apart and makes you stand out in your industry.

- Learn the best ways to market your business: Because market research helps you learn more about your customers, you can find the best ways to sell to them. Are they on social media, or more likely to consume traditional print media? Are billboards more likely to bring in new customers, or should you invest your marketing budget into email? Learning about your potential customers will help you answer these questions.

Step 3: Create a business plan

Now that you’ve tested your idea through market research, it’s time to take everything you’ve learned and create a business plan.

A business plan is a written document that defines your business and outlines your business strategy, future goals, and how you plan to reach those goals. Think of your business plan as the map that’ll get you from Day 1 to Day 1,438 as a business owner.

Every business should have a business plan. A lot of people assume that business plans are only for those looking for outside funding from investors or a bank. But every business can benefit from a business plan—it can help you expand on your business idea and uncover any potential issues you may have overlooked. Even if you’re not starting out, but say, looking at a second location, a business plan is an important step to validate your decisions.

Business plan essentials

Every business plan is different, but you can feel confident that you’ve created a well-rounded business plan if you include the following sections:

- Executive summary: Think of this as a paragraph or two that condenses everything you’ve written in your business plan. While this should be the first part of your business plan, most people leave it as the last thing they write.

- Company description: What is your business? What problem are you solving? Why is your solution to this problem the best on the market? These are the questions you should be answering in your company description.

- Market analysis: Here’s where your market research comes into play. This section is where you position your business against competitors. It should include your target market, market size, growth rate, trends, etc.

- Mission and goals: It’s time to start thinking about your business’s mission. Include a brief mission statement and outline what you hope to achieve as a business. Make sure the goals you include are SMART goals.

- Products or services. This section outlines how your business operates. Are you selling a product or offering a service? Get into the details and include what you’ll offer, how much it costs, who creates the product/provides the service, and how much overhead you have.

- Background summary: Here’s where you’ll include all the historical data, research, and articles you’ve collected. Summarize this information and outline how your findings will positively or negatively affect your business or industry.

- Marketing plan: How will you promote your business? This section of your business plan should outline your unique value proposition, marketing campaign plans, and the expected cost for all marketing efforts.

- Financial plan: Arguably the most important part of any business plan. Afterall, without money, it’s unlikely you’ll have much of a business. This section often includes a proposed budget and projected financial statements for five years, like a balance sheet, cash flow report, and income statement. This is where you outline any funding requests you’re seeking.

Step 4: Finance your small business

Now that all your ideas are on paper, it’s time to think about how you’ll finance your small business. Depending on the type of business you’re opening, you may be looking at anywhere from a few thousand dollars to a few hundred thousand dollars to get started. The average cost for a small business to start and run for their first full year is $40,000.

No matter what your start-up costs are projected to be, don’t let this stop you yet. There are lots of funding options available to small businesses, including:

- Self-funding or bootstrapping: A lot of small businesses start off using their personal funds. But if your financial needs are high, there’s a lot of financial risk that comes with bootstrapping your business.

- Small business loans or lines of credit: There are a lot of great small business loans and lines of credit that you can use to get your business off the ground. You’ll need your business plan along with personal financial statements when you apply.

- Small business grants: Small business grants provide funding you don’t have to pay back. It can take some time to research and apply for grants, but it can be worthwhile if you can secure a grant. Check out some of the grants offered by the Small Business Administration here.

Step 5: Decide on your business structure

Choosing a business structure isn’t a decision that should be made lightly. How you structure your business will affect the tax you owe, your daily operations, and the personal risk you assume, and may have other legal implications down the road.

Here’s a rundown of the most common business structures:

Sole proprietorship is the most common business structure for solo entrepreneurs. In this business structure, the company and the owner are considered the same. Therefore, if the business fails, the owner is personally responsible for all business debts.

Partnerships are used when starting a business with more than one individual. A partnership requires a partnership agreement, and partners have limited liability for the debts of the LLP.

Limited liability companies or LLCs can be owned by one or more people/companies and limit your personal liability for business debts. They’re one of the easiest business structures to establish.

Cooperatives are businesses or organizations that run to benefit those using the services. Industries that fall into this category include, but aren’t limited to, health care, retail, restaurants, and agriculture.

Corporations are more complex from a legal and tax point of view. Because of this, they’re more common in larger companies but can still be used by small businesses.

Consider speaking with a lawyer or accountant before deciding to ensure you’re making the best decision for your business.

Step 6: Dig into the legal must-haves

It’s important to dot your i’s and cross your t’s when it comes to the legal ins and outs of a small business. And there are a lot of i’s and t’s to keep track of. When you’re starting a new small business, make sure you have the following in order before you begin operating:

- Register your small business: While it’s not always necessary to register your small business at a federal, state, or local level, doing so may help with your personal liability protection, and it may have some legal and tax benefits.

- Apply for an employer identification or tax I.D. number: Your employer identification number (EIN) is issued by the IRS. You need one so you can file federal taxes, hire employees, and open a business bank account. You can apply for an EIN on the IRS website. Some states also require a state-level tax I.D. number, so check if one is needed in your state.

- Insure your small business: Even if you’re a home-based business or don’t have any employees, you need to have insurance for your small business. The kind of insurance you need depends on your business model and what risks you—and your customers—may face. Reach out to an insurance agent to get the full scoop on what kind of insurance is best for your business.

- Open a business bank account: When you start a business, you need a separate bank account to accept payments, pay employees, and make business purchases. What kind of bank account is best depends on your business needs. Start exploring the banks in your area to find one that meets your needs.

Step 7: Get the right tools to run your small business

Finding the right tools to run your small business is key to helping your business run smoothly. The right business tools will save you time and money and make you a desirable employer. The tools you need will depend on your small business, but looking for tools that automate repetitive tasks and lessen your workload is a great place to start.

With Homebase, you get everything you need to take control of your business. Designed for hourly work, Homebase will help you schedule your team, track their hours, and run payroll seamlessly. You’ll also have a team communication app that keeps you and your employees on the same page. Homebase even has expert H.R. guidance to help you comply with government regulations without an in-house H.R. team.

Homebase is the all-in-one management app that simplifies running your small business. Get started now for free.

How to start a small business FAQs

How much does it cost to open a small business?

It costs the average small business $40,000 to start and run for an entire year. This number depends on many factors, including what kind of business it is, if you need real estate to operate, and if you have employees. Some home-based businesses can start with just a few hundred dollars, whereas starting a restaurant can cost hundreds of thousands of dollars.

What’s the best business structure for a small business?

The best business structure for your small business depends on various factors. What kind of business are you forming? What industry are you in? Are you the only owner? A successful business structure protects you and your employees and allows you to set realistic goals and follow through on your plan to reach those goals.

Do I need a license to start a small business?

Whether or not you need a license to start your small business depends on the type of business you’re starting and where you’re located. For example, to open a daycare, you’ll need to get a license, but the requirements vary depending on your state. Spend some time researching your business and the licenses required to run a business in that industry in your state.

Remember: This is not legal advice. If you have questions about your particular situation, please consult a lawyer, CPA, or other appropriate professional advisor or agency.